RMB Rising: Challenges and Implications of the Renmibi's Internationalization for China and the Global Economy

Spring 2023

I. Introduction

In recent decades, the People's Republic of China has rapidly emerged as a global economic powerhouse, transitioning from a low-income, predominantly agrarian economy to become the world's second-largest economy, and a dominant player in international trade and finance. Central to this unprecedented economic transformation is the Renminbi (RMB), China's national currency, which has increasingly gained prominence in global financial markets. RMB internationalization— the expanding acceptance and usage of the RMB for cross-border transactions, investments, and reserve holdings— has captured the attention of academics and policymakers alike due to its potential to reshape the global monetary landscape and alter power dynamics within the world economy.

Initially, it is essential to define the term "RMB internationalization," which refers to the process where the RMB achieves greater recognition and acceptance beyond China's borders, assuming an influential role in global trade and finance. Though there is no universally agreed-upon indicator to measure RMB internationalization, critical facets include its usage in trade settlements, international financial transactions, offshore RMB centers, and central bank reserve holdings.

The significance of RMB internationalization extends beyond China's domestic economy. It has the potential to recast the international monetary system, altering global trade and capital flow dynamics, while also impacting exchange rates, interest rates, and financial stability across various economies. Of particular interest is the increasing possibility of the RMB challenging the long-standing supremacy of the U.S. dollar as the dominant global reserve currency, transforming the prevailing economic and political order. Moreover, RMB internationalization is intrinsically tied to both China's financial market liberalization and the broad-ranging economic and political goals pursued by the Chinese leadership, rendering it a matter of strategic importance for both China and the international community.

This paper aims to examine the multifaceted dimensions of RMB internationalization, providing an in-depth analysis of its evolution, current state, and potential future trajectories. By evaluating the key policies, initiatives, and market developments that have shaped China's efforts to internationalize the RMB, we intend to elucidate the primary challenges and opportunities characterizing this process and the implications it holds for China's macroeconomic management, financial reforms, and geopolitical ambitions. Assessing the broader ramifications of RMB internationalization on the global economy constitutes a crucial aspect of this research endeavor, as we strive to understand and interpret the growing role of the RMB within the shifting dynamics of the international monetary system.

II. Progress of RMB Internationalization

A. Policy Measures

The Chinese government has adopted an array of policy measures aimed at facilitating the internationalization of the RMB since the early 2000s. In fact, “the PBoC started planning the internationalization of the RMB in 2006 at the latest, but the pace of actual implementation picked up amid the global financial crisis, which raised the possibility of the weakening of the role of the U.S. dollar and a demand for an alternative international currency” (Eichengreen and Kawai). These relatively modern measures can ultimately be classified into three broad categories: capital account liberalization, exchange rate regime reform, and the development of offshore RMB markets.

A key prerequisite to RMB internationalization is the liberalization of China's capital account, allowing for increased cross-border capital flows. Historically, China has maintained strict capital controls, with stringent regulations governing the inflow and outflow of funds across borders. However, more recently, China's government has implemented several schemes allowing for controlled and calibrated opening of the capital account to both inflows and outflows. One key measure is the expansion of quotas for Qualified Foreign Institutional Investors (QFII), which was introduced in 2002 to give foreigners limited access to the renminbi-denominated securities markets. As of mid-2013, there were 207 qualified foreign institutional investors with an approved quota of US$43.5 billion (Eichengreen and Kawai). Another significant initiative is the RMB Qualified Foreign Institutional Investors (RQFII) program, which was launched in 2011 and allows qualified investors to invest in the PRC securities markets using the renminbi from offshore markets. As of mid-2013, there were thirty RQFIIs with approved quotas (Eichengreen and Kawai). These initiatives have eased foreign investors' access to China's financial markets and promoted the increased usage of RMB in cross-border transactions.

An additional essential aspect to China’s internationalization of the RMB comes with their approach to exchange rate regime reform. Recognizing the importance of a more market-determined exchange rate in promoting the RMB, China has undertaken significant reforms to its exchange rate regime over the past few years. The transition began in 2005 with the decision to end the fixed exchange rate system, which pegged the RMB to the U.S. dollar, and move towards a managed floating exchange rate regime, linked to a basket of currencies. Further steps have been taken in recent years to enhance the market-driven nature of the exchange rate, such as the widening of the daily trading band and the adoption of a more transparent midpoint fixing mechanism by the People's Bank of China (PBoC) (Subramanian and Kessler). These exchange rate regime reforms have enhanced the credibility of the RMB valuation and fostered greater confidence in its use as an international currency.

Increased flexibility in the RMB's value against other currencies, such as the U.S. dollar, and foreign exchange market interventions have been crucial in maintaining economic stability in China during periods of market uncertainty. As the RMB continues to float more freely in international markets, central banks worldwide have increased their holdings of RMB-denominated assets, cementing the currency's role as a key reserve asset in global finance (Eichengreen and Kawai). Furthermore, the implementation of a managed floating exchange rate regime and the internationalization policy have bolstered the RMB's influence on other currencies, particularly in emerging East Asian economies. The ongoing reforms in China's exchange rate regime and their connections to the broader process of RMB internationalization underline the importance of strategic cooperation and policy coordination between China and the international community.

The final vital aspect of RMB internationalization is the creation of offshore RMB markets, which enable the use of RMB outside mainland China for financial transactions, investments, and deposits. These centers have contributed to the growth of the offshore RMB market by offering a range of RMB-denominated financial products and services, including RMB-denominated bonds (known as 'Dim Sum' bonds), RMB loans, and RMB deposits.

An important element in the success of offshore RMB markets is the establishment of bilateral swap lines between the PBoC and other central banks worldwide, which have become one of PBoC's signature policies for promoting RMB internationalization (IMF 2021). As illustrated in Figure 1, the geographic coverage of swap lines began with neighboring Asian countries, later expanding to include emerging markets, as well as advanced economies such as Canada, the European Central Bank, and the United Kingdom. These advanced economies have signed swap lines with the PBC primarily to address potential financial stability risks (Figure 1).

The Chinese government has supported the expansion of the offshore RMB markets by signing currency swap agreements with foreign central banks, providing RMB clearing arrangements, and allowing direct conversion between the RMB and various foreign currencies (Subacchi and Huang). The development of offshore RMB markets—enabled and supported by the Chinese government as well as international financial centers like Hong Kong, Singapore, and London—has been instrumental in advancing the RMB internationalization process. As these markets continue to grow and diversify, they will play a crucial role in enhancing the acceptance and use of the RMB in the global economy.

B. Indicators of International Usage

To assess the extent of RMB internationalization, it is essential to examine a range of indicators that reflect the currency's expanding global usage in trade, finance, and official reserves. These indicators provide valuable insight into the progress of RMB internationalization over time and offer a benchmark to compare its standing against other major international currencies.

One crucial indicator of RMB internationalization is its growing status as a reserve currency and its inclusion in the International Monetary Fund's (IMF) Special Drawing Rights (SDR) basket. As the RMB gains recognition as a reserve currency, central banks worldwide include RMB-denominated assets in their foreign exchange reserves. This increased allocation of RMB assets not only strengthens the currency's international legitimacy but also reflects the growing confidence in its long-term stability and value. Additionally, the RMB's inclusion in the IMF's SDR basket in 2016 signaled the currency's increasing global prominence and the substantial economic and financial reforms that China undertook. Being part of the SDR basket enhances the RMB's credibility, encourages its use in international financial transactions, and ultimately serves as a significant indicator of the currency's ongoing internationalization journey (Prasad).

Another key indicator of RMB internationalization is its share in global trade and financial transactions. As mentioned earlier, RMB-denominated trade settlement has grown rapidly, accounting for approximately 23% of China's total foreign trade as of 2023. This development highlights the currency's increased use in facilitating cross-border transactions, which is a fundamental aspect of the internationalization process (Figure 2).

Similarly, examining RMB's share in global financial transactions provides further evidence of the currency's expanding international presence. According to SWIFT, a global provider of secure financial messaging services, RMB's share in global payments increased from 1.89% in 2014 to a pre-Covid peak of 3.20% in January 2020. Presently, it still sits at 2.19% making it the fifth most-used currency for international payments (Figure 3). At the same time, the figure illustrates China’s uphill battle in shaking the international monetary status quo, indicating a necessary further progression of growth measures.

III. Challenges for RMB Internationalization

A. Domestic Financial Market Reforms

While the RMB has made impressive strides in its internationalization journey, the path forward is not devoid of challenges. A key set of challenges lies in the realm of domestic financial market reforms, as achieving RMB internationalization necessitates a holistic and well-coordinated approach to address the underlying structural issues in China's financial system. The main areas of concern in this regard are interest rate liberalization, capital market deepening, and regulatory framework and supervisory capacity.

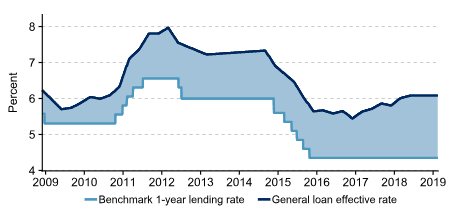

To fully realize the potential of RMB internationalization, China needs to continue liberalizing its interest rate regime, allowing market forces to play a decisive role in determining interest rates. Historically, “the interest rate policy of the PBoC has limited influence on the economy’s interest rate structure as a whole, thereby limiting the ability of China’s monetary authority to take full advantage of the quick response of the interest rate resulting from a more international use of the renminbi” (Gao and Yu; Figure 4).

Interest rates on bank deposits and loans have been completely liberalized since 2015, although the PBC continues to establish reference rates. In addition, the government has shifted from implicitly backing all bank deposits to implementing an explicit deposit insurance system. This change subjects even state-owned banks to increased market discipline, as depositors are now more inclined to scrutinize the financial health of banks where they hold savings. However, in order to ensure stability and resilience in China’s financial markets, there must be some ways to go. Numerous regulatory gaps persist across various sectors of the financial system, while escalating corporate debt and the expansion of the shadow banking system pose threats to financial stability (Prasad).

Another major challenge for RMB internationalization is the deepening and broadening of China's domestic capital markets. China's capital markets are relatively underdeveloped compared to the advanced economies, marked by the predominance of bank-based financing, limited diversity of financial products, and low levels of institutional investor participation. Each reserve currency has historically gained global significance under unique circumstances, driven by various motivations; however, a consistent requirement is the presence of financial markets capable of accommodating diverse and substantial demands from both private and official foreign investors (Prasad).

In order to facilitate RMB internationalization, China needs to deepen its capital markets by diversifying financial instruments, encouraging the growth of institutional investors, and permitting greater market access for foreign investors. While progress has been made through China’s 2002 Qualified Foreign Institutional Investor program (CFII) and the 2007 Qualified Domestic Institutional Investor scheme, which both opened up the domestic capital market through standardization and the liberalizing of institutional investment, their financial markets still require further expansion. (Gao and Yu) A deeper and more liquid capital market would enhance the capacity of China's financial system to absorb capital inflows, support the growth of the offshore RMB market, and provide attractive investment opportunities for international investors, thereby propelling RMB internationalization (Eichengreen and Kawai).

B. External Factors

In addition to domestic financial market reforms, several external factors present challenges for RMB internationalization. These challenges underscore the complexity of the process and the broader implications beyond China's borders. The primary external factors encompass geopolitical tensions and trade disputes, as well as global economic uncertainty.

Geopolitical tensions, such as the trade war between the United States and China, significantly impede the RMB's internationalization prospects. The trade war has led to a series of tit-for-tat tariff measures, impacting various industries and instigating a slowdown in global trade (Figure 5). As China's global influence grows, the rivalry with the United States has also manifested in technology and intellectual property rights disputes and national security concerns. The ongoing trade war and associated tensions directly impact RMB internationalization by slowing down China's trade relations and creating uncertainties in the global economy. This situation makes international investors more cautious, potentially discouraging foreign investment in China's financial markets, and fostering distrust in the RMB's stability and credibility as an international currency. Additionally, the trade war's ripple effect has extended into other bilateral issues between the United States and China, further fueling a negative environment for RMB internationalization. With the world closely watching China's approach, especially in its ongoing contest with the United States, RMB acceptance abroad and the internationalization efforts face significant challenges. (CSIS)

Prevailing global economic uncertainty can adversely impact RMB internationalization efforts. Conditions such as economic crises, political instability, and fluctuations in commodity prices can lead to heightened investor risk aversion. Investors may prefer allocating resources to safe-haven assets, such as U.S. dollar-denominated debt, rather than RMB-denominated assets. Moreover, global economic uncertainty can result in volatile capital flows and exchange rate fluctuations, making it challenging for the RMB to gain and maintain its position as a preferred currency for trade, investment, and reserve holdings.

IV. Economic Implications of RMB Internationalization

For China, RMB internationalization brings numerous potential benefits. Among the key advantages are enhanced monetary policy autonomy, reduced reliance on the U.S. dollar, and financial market development and integration.

Firstly, RMB internationalization can lead to greater autonomy in China's monetary policy. As the RMB assumes a more prominent role globally, it reduces China's susceptibility to external shocks and allows authorities to have more control over domestic economic conditions. Through RMB internationalization, the PBoC could have a broader range of policy tools at its disposal, enabling it to better manage issues such as inflation, economic growth, and financial stability.

Moreover, the rise of the RMB in international trade and finance holds the potential to reduce China's dependence on the U.S. dollar. Presently, due to the dominant position of the U.S. dollar in global finance, China's foreign trade transactions and external debt largely rely on dollar-denominated transactions. This leaves China susceptible to fluctuations in the U.S. dollar's value and the possible consequences resulting from shifts in U.S. monetary policy. By promoting the RMB's stature on the international stage, China can lower its vulnerability to exchange rate risks and temper the effects of worldwide economic fluctuations. In fact, when the dollar undergoes depreciation for extended periods, OPEC occasionally considers adopting an alternative currency as the denomination standard. Although this switch has yet to occur, it could potentially take place if the dollar's supremacy in other international roles were to be seriously undermined (Frankel).

Lastly, RMB internationalization can spur the development and integration of China's financial markets. By promoting capital account liberalization and deepening domestic capital markets, China can attract greater foreign investment and foster the growth of diverse financial products, thereby enhancing the efficiency and maturity of its financial system. In addition, as some researchers have argued, RMB internationalization will largely benefit the rise of Shanghai as an international financial center (Gao and Yu 2010). Furthermore, RMB internationalization may actually become a new catalyst for financial reform if PRC authorities believe that a more internationalized currency is in the national interest (Eichengreen and Kawai).

The economic implications of RMB internationalization also extend to the global economy, with potential consequences in areas such as the shift in global currency composition and the diversification of reserve assets held by central banks worldwide. As the RMB becomes a prominent international currency, and as the costs of transacting in the RMB and other emerging market currencies fall, the dollar's prominence as a unit of account (for denominating trade transactions) and as a medium of exchange (for settlement of cross-border financial trade and financial transactions) will decline (Prasad).

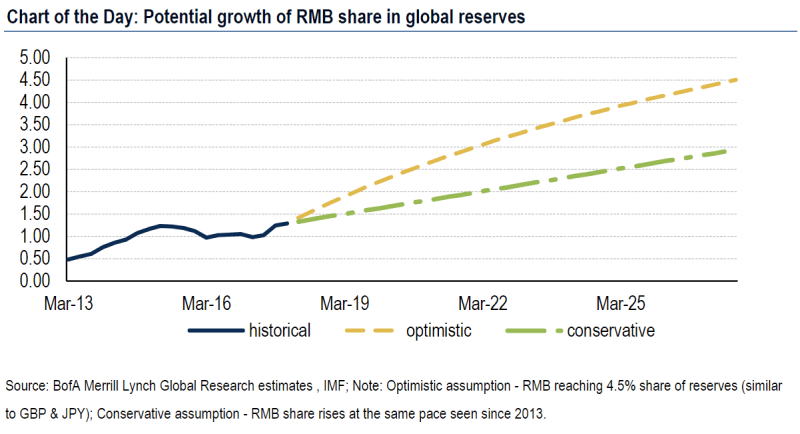

A related implication is the potential for increased diversification of reserve assets held by central banks worldwide. There is no clear guidance from economic theory about how many currencies would be best for a world economy that is becoming increasingly closely integrated (Prasad). However, as the RMB grows more entrenched as an international currency, central banks may diversify their reserve portfolios by including a larger share of RMB-denominated assets. The inclusion of the RMB in the International Monetary Fund's Special Drawing Rights basket in 2016 already signaled its growing importance as a potential reserve currency. By diversifying reserve assets, central banks can reduce their exposure to the risks associated with a single currency, which may have beneficial effects on global financial stability (Figure 6).

V. Policy Recommendations

A. For the Chinese Government

To further promote RMB internationalization and maximize the potential economic benefits of this process, it is crucial for the Chinese government to undertake a series of proactive measures. These measures include further integrations of financial market reforms, strengthening of macroeconomic management, and enhancing international cooperation.

First and foremost, promoting RMB internationalization involves progressing financial market reforms within China. Building on previous achievements, the Chinese government should implement specific measures, such as gradually introducing a market-driven interest rate system by phasing out government controls like lending rate floors and deposit rate ceilings. This will enhance resource allocation efficiency and financial stability (Eichengreen and Kawai). Additionally, expanding and diversifying capital markets will create a more robust financial market, offering a broader range of investment opportunities and increasing the appeal of RMB-denominated assets.

Emphasizing increased transparency, predictability, and consistency within the regulatory framework is also crucial. Streamlining processes and aligning policies with international best practices will create a welcoming environment for both domestic and international investment. Strengthening regulatory agencies is essential, including capacity building, personnel training, technology infrastructure upgrades, and adopting best practices from international counterparts. By first implementing these measures, China can foster an investor-friendly environment, instill confidence, and mitigate risks related to RMB internationalization.

Thus far, in terms of geopolitical cooperation and expanded policy dialogue, the Chinese government has already begun to adopt a more accessible stance. They’ve displayed an active participation in multilateral forums, such as the Group of Twenty and the Asian Infrastructure Investment Bank, as well as establishing closer ties with Asian trading partners through the $40 billion Silk Road infrastructure fund. Easing of international stressors and seeking foreign cooperation will allow China to diversify its foreign investment allocations beyond traditional investments, yielding better economic returns and also an intangible but substantial payoff in terms of increased influence in Asia and beyond (Prasad).

The importance of geopolitics in currency internationalization cannot be understated. As seen from the experiences of the Deutsche Mark, Japanese Yen, and the Euro, China’s inability to match lucrative trade alliances and security guarantees provided by Washington was a political deterrent enough to dissuade global trends away from the adoption of these currencies (Frankel). However, that is not to say that the RMB’s international usage status necessitates a hegemonic ‘big stick’ reactionary policy. In fact, the internationalization of the RMB has undoubtedly been only impeded by China's communist political structure and rapid military expansion, such as the growing presence and aggression in the South China Sea, with its neighbors.

In light of the aforementioned factors, several policy measures are suggested for China to work on its international relations and achieve the RMB's internationalization. These include strengthening regional security partnerships, as demonstrated by China's participation in multilateral military exercises like RIMPAC; promoting regional economic integration through initiatives like the Belt and Road Initiative (BRI) and the Regional Comprehensive Economic Partnership (RCEP); increasing financial and economic transparency, for instance by adopting international regulatory standards and increasing transparency in the allocation of loans in the BRI; and encouraging RMB usage in regional trade and investment, evidenced by the growing number of RMB-denominated transactions in countries like Singapore and the United Kingdom (Gao and Yu).

By fostering trust, cooperation, and transparency with neighboring countries and the international community, China can create a more conducive environment for the RMB to succeed in global finance. These concerted diplomatic efforts and strategic policy measures will be critical in ensuring the internationalization of China's RMB, as economic prowess alone cannot guarantee its success at the global stage.

B. For the International Community

To further RMB internationalization, the international community should aid China in integrating its financial markets into the global economy as they would see economic benefits themselves. For one, this support can contribute to global economic growth by capitalizing on the potential of China's economy, which sits as the world's second-largest. Secondly, backing initiatives like the Stock and Bond Connect programs can present international investors with new investment opportunities through facilitated access to China's growing capital markets; an opportunity to diversify portfolios and gain exposure to a broad array of sectors and industries, leading to improved risk management and better returns (Eichengreen and Kawai). Furthermore, incorporating China into the global financial markets can encourage financial innovation and competition, benefiting both the domestic and international market participants. This integration process can foster collaboration among financial institutions and regulators to develop and adopt best practices, enhance risk management capabilities, and accelerate the adoption of cutting-edge financial technologies.

In order for the easement of China into the global financial network, the big players within it hold a share of the burden in the transition process. The international community needs to engage China in targeted bilateral or multilateral dialogues that address specific challenges in liberalizing its financial markets. There should be a priority placed on key aspects, such as easing restrictions and promoting a level playing field for both domestic and foreign financial institutions. For instance, implementing hybrid instruments and allowing more flexibility in interest rates in order to improve risk sharing and capital allocation efficiency.

Furthermore, encouraging transparency and adherence to international financial standards are vital for China's successful integration. In this regard, international cooperation efforts should concentrate on aligning China's regulatory frameworks with best practices worldwide. A well-regulated environment that follows standards such as the International Financial Reporting Standards (IFRS) and Basel III regulations will instill confidence in foreign investors and ensure China's financial stability, leading to more effective engagement in global markets.

The international community should additionally support the RMB's internationalization by selectively promoting its use in specific financial products and regional trade, focusing on areas where the RMB has a competitive advantage or aligns with regional economic development. For example, incentivizing regional projects in Asia, particularly in countries participating in China's Belt and Road Initiative, to increasingly adopt RMB, will boost its prominence in global finance.

VI. Conclusion

Our findings indicate that significant progress has been made in RMB internationalization, driven by a combination of policy measures - such as capital account liberalization, exchange rate regime reform, and the development of offshore RMB markets - and market developments, including the growth of RMB-denominated trade settlements, financial products, and RMB's status as a reserve currency. Moreover, we have identified various indicators of international usage that illustrate the growing acceptance and use of the RMB in the global economy, such as its share in global trade and financial transactions and its 2016 inclusion in the IMF's Special Drawing Rights basket.

Despite this progress, RMB internationalization faces several challenges, both domestically and externally. Domestic challenges encompass further financial market reforms, including interest rate liberalization, capital market deepening, and strengthening of the regulatory framework and supervisory capacity. External challenges are chiefly related to geopolitical tensions and trade disputes, competition with established reserve currencies, and global economic uncertainty. Addressing these challenges will be crucial for the continued advancement of RMB internationalization.

In terms of economic implications, RMB internationalization carries significant consequences for both China and the global economy. For China, potential benefits include enhanced monetary policy autonomy, reduced reliance on the U.S. dollar, and accelerated financial market development and integration. The global economy, meanwhile, may experience shifts in global currency composition, increased diversification of reserve assets, and potential impacts on global economic stability.

Finally, the analysis and findings presented in this research paper highlight the significance of RMB internationalization not only as a subject of academic study but also as a critical issue for economic policymakers and market participants. Understanding the process of RMB internationalization, its challenges, and implications can improve our comprehension of global economic developments and inform strategic decision-making at both the national and international levels.

VII. Figures

References

- Chatham House. Subacchi, Paola, and Huang Haizhou. "The Connecting Dots of China’s Renminbi Strategy: London and Hong Kong." Chatham House Briefing Paper, 2012, https://www.chathamhouse.org/.

- Eichengreen, Barry, and Masahiro Kawai. "Issues for Renminbi Internationalization: An Overview." Journal of International Commerce, Economics, and Policy, vol. 5, no. 1, 2014.

- Frankel, Jeffrey. "Internationalization of the RMB and Historical Preconditions." Journal of Economic Integration, vol. 26, no. 3, 2011, pp. 430-465. doi: 10.11130/jei.2011.26.3.430.

- Gao, Haihong, and Yanyan Yu. "Internationalization of the Renminbi: Pathways, Implications, and Opportunities." China-US Focus, 2012, https://www.chinausfocus.com/finance-economy/internationalization-of-the-renminbi-pathways-implications-and-opportunities.

- International Monetary Fund (IMF). "International Financial Statistics." http://www.imf.org/.

- Knoema. http://www.knoema.com/.

- MarketWatch. https://www.marketwatch.com/.

- People's Bank of China. (Various years). China Monthly International Finance. Retrieved from http://www.pbc.gov.cn/

- Prasad, Eswar S. "China's Efforts to Expand the International Use of the Renminbi." Brookings Institution Report, 2016, https://www.brookings.edu/wp-content/uploads/2016/07/RMB-paper-final.pdf.

- Subramanian, Arvind, and Martin Kessler. "The Renminbi Bloc is Here: Asia Down, Rest of the World to Go?" Working Paper 12-19, Peterson Institute for International Economics, 2012, https://www.piie.com/publications/wp/wp12-19.pdf.

- SWIFT. https://www.swift.com/.